If you've ever searched for a budgeting method and immediately felt tired, you're not alone. Most budgeting advice asks you to track every dollar, build a dozen categories, and check in constantly. Most people try it for two weeks and quietly give up.

The 50/30/20 rule is different. It's the closest thing personal finance has to a back-of-the-napkin shortcut — one you can hold in your head without ever opening a spreadsheet. Here's how it actually works, where it falls apart, and how to use the idea without turning money into a part-time job.

Want to see where your own money actually goes? Try Spendalyst free for 14 days →

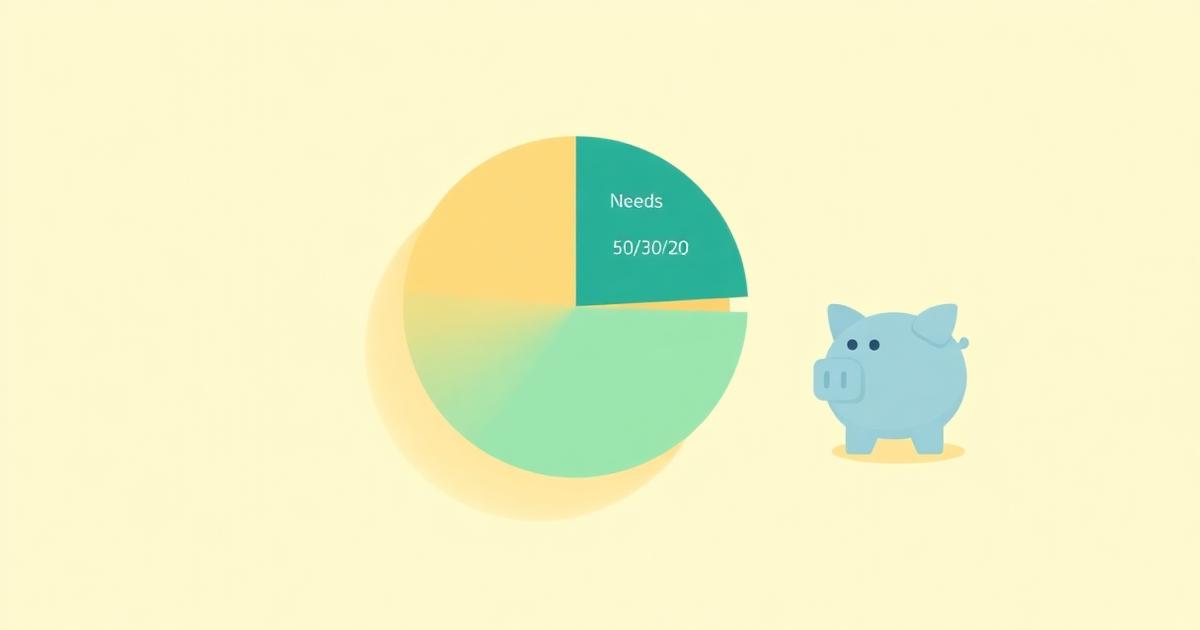

What the 50/30/20 rule actually says

The rule splits your after-tax income into three buckets:

That's the whole thing. If you take home $4,000 a month, that's roughly $2,000 for needs, $1,200 for wants, and $800 toward savings or debt.

The reason it caught on is simple: it's a sense of proportion, not a set of rules. You're not assigning every coffee to a category. You're just checking whether the big shape of your spending is roughly sane.

Why it works when stricter budgets don't

Traditional budgets fail for a reason we've written about before — they ask for ongoing effort that real life doesn't leave room for (this is why most budgets fall apart). The 50/30/20 rule sidesteps that by being forgiving on purpose.

It works because:

Where the rule breaks down

It's a useful starting frame, not gospel. A few honest caveats:

If the percentages don't fit your life, adjust them. 60/20/20 or 50/20/30 are perfectly reasonable. The buckets matter more than the exact split.

How to use it without becoming a spreadsheet person

Here's the part most articles skip. You don't have to manually sort transactions to use this rule. You just need to know, roughly, where your money already goes — and then compare it to the 50/30/20 shape.

The hard part has never been the math. It's seeing where your money actually went without spending a Sunday afternoon adding things up. Once you can see your spending broken into needs, wants, and savings automatically, the 50/30/20 rule stops being a chore and becomes a quick gut check: *Am I roughly in balance? If not, which bucket is out of line?*

That's the whole game. Awareness first, adjustments second.

A worked example: the 50/30/20 rule on a real paycheck

Numbers make this concrete. Say you take home $3,500 a month after tax. The rule gives you:

Now imagine the real version, where it's a little off. Your rent is actually $1,400 in a pricey city, so needs are closer to 57%. That's the useful signal: your housing is the lever, not your coffee. You might trim wants to 25% to keep savings at 20%, or accept a 55/25/20 split for now and revisit when your lease is up. Either way, you spotted the real issue in about thirty seconds — which is the entire point of the rule.

Frequently asked questions

Is the 50/30/20 rule actually good? It's a good starting framework, especially if stricter budgets have never stuck for you. It gives you a sense of proportion without demanding daily tracking. It's less precise than a zero-based budget, but for most people "directional and sustainable" beats "exact and abandoned."

Should I use gross or net income? Net (after-tax) income — the amount that actually hits your account. Taxes are already spoken for, so budgeting off your gross salary would overstate what you have to work with.

What counts as a "need" vs. a "want"? A need is something that has real consequences if you skip it: housing, basic food, utilities, transportation to work, insurance, minimum debt payments. A want is everything that improves life but isn't essential — dining out, streaming, hobbies, upgrades. A useful test: if losing it would only be uncomfortable, it's a want; if it would be a genuine problem, it's a need.

What if my needs are more than 50% of my income? Very common, especially with today's rents. Don't force it — adjust the split (say 60/20/20) and treat the high number as information. Persistently high needs usually point to housing or transportation, the two biggest levers, rather than to small daily spending.

Does the 50/30/20 rule work for low or irregular income? The percentages are harder to hit on a tight or variable income, but the shape still helps. For irregular income, average your take-home over the last three months and apply the rule to that average rather than any single paycheck.

How is this different from a normal budget? A traditional budget assigns nearly every dollar to a specific category you then have to police. The 50/30/20 rule only asks about three broad buckets, so it fits in your head and survives real life. It's a compass, not a cage.

The takeaway

The 50/30/20 rule is the least painful framework in personal finance because it asks for proportion, not perfection. Use it as a rough compass: half your money keeps the lights on, a third makes life enjoyable, and a fifth builds your future. If one bucket is badly out of shape, that's your signal — not a reason to feel guilty.

You don't need a stricter system. You need a clear picture and one honest question each month. The rest takes care of itself.

Spendalyst shows you where your money actually goes — sorted, in plain English, no budgeting spreadsheet required. See your real spending picture in 60 seconds.